Framing (historical costs attached)

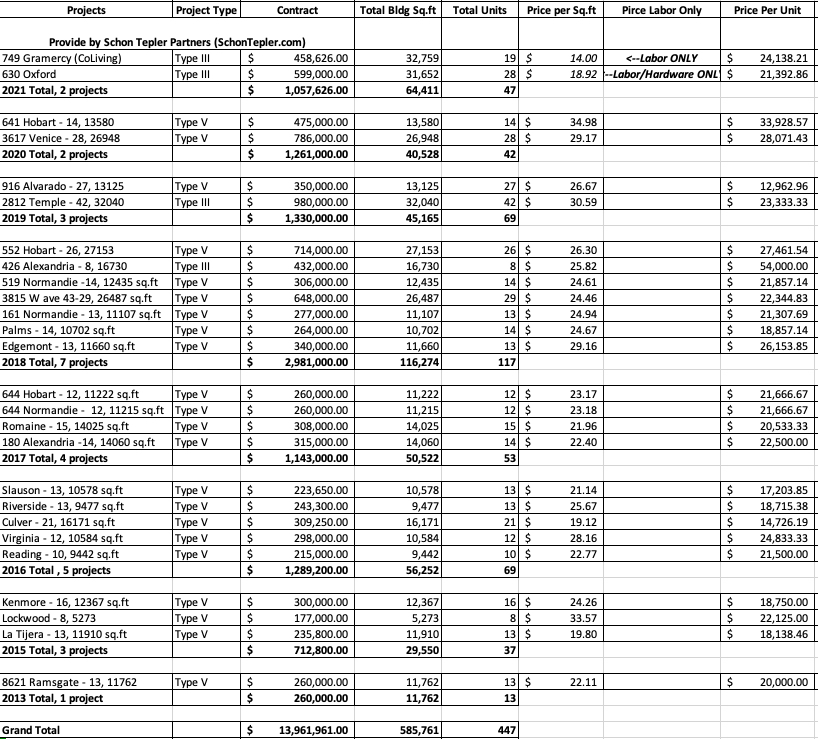

FRAMING -"The Bones" of the building: (attached pic is our historical costs) In low/mid-rise apartment construction, framing is typically made from wood. Wood is reinforced with different types of hardware, such as Hardie frames and earthbound systems, and sometimes structural steel. The amount of hardware and structural steel used depends on the specific project and the engineer designing the building. Type V is the simplest type of wood construction, and most single-family homes and buildings up to 4 stories are typically Type V.

Type III construction is typical on projects with 5 stories or more of wood. It uses more fire-treated lumber and has DensGlass on the exterior of the building because it has a high fire resistance rating. The fibers in the DensGlass are made of gypsum, which is a naturally fire-resistant material, and the fibers are also treated with fire-retardant chemicals to improve its fire resistance. Type III construction in the past was 20-30% more expensive on the framing and drywall line items compared to Type V.

We've never built or framed buildings outside of Los Angeles, but I would assume there would be less hardware required in framing in other states. The building codes in Los Angeles are strict to protect against earthquakes.

The cost of framing has the following components: Labor for Framing Insurance for Labor Lumber Cost Hardware Cost Equipment Rental and Fuel Profit & Overhead (15%-20%) Total Bid Price

Pre-covid, our costs were in the $24-26 per square foot range on mostly Type V projects. I've never had it broken out, but my understanding is that it was roughly $8-10 for labor, and the rest was for hardware, profit, and overhead.

However, during the COVID-19 pandemic, that number changed significantly. While labor costs remained roughly the same, lumber prices doubled and tripled, leading to huge unexpected increases in price.

Framers refused to bid on both lumber and labor and started bidding just either labor or just labor and hardware. The lumber risk was shifted onto the developer.

Framers did not honor their contracts, and I did not expect them to go broke for what could be called an act of God (or act of Fauci). Many walked away from their contracts, leaving General Contractors to work it out with their developers. We had to work it out with ourselves.

Now, many GMP contracts and framing contracts have exclusions for drastic cost increases in materials. Framers/GCs are not commodity traders and should not be expected to bear that risk. The cost of lumber has come back to earth, but as of today, it's still above pre-covid levels

The commodity risk has been shifted to the developer. When possible, developers buy out their lumber early. The issue with building infill development is when buying it early, there's no place to store it and now you have to price in the storage and transportation of the lumber versus the risk of its price going up. Please share this thread on Framing by retweeting if you find it useful.